The one concept crypto promoters are afraid to understand

And why they should embrace it

Since I began this newsletter I’ve produced a number of pieces intended to help readers see through the topsy-turvy mythologies that surround crypto-tokens. I don’t do this to ‘diss’ crypto projects*, or to mock the people who believe in their potential. A person who ‘calls a spade a spade’ is not dissing spades, but they are a threat to those who call a spade a golden sword. Likewise, the fact that I wish to call a spade a spade when it comes to crypto-tokens does not make me a crypto sceptic. I have respect for the actual capabilities of various crypto systems, but my work can threaten those those who spend their days presenting crypto-tokens as a golden sword that will slay the incumbent monetary system.

So, in the spirit of celebrating the spade-ness of spades, let’s dive into this new piece. I’m going to show how the promoters of many crypto projects try to mix categories that are typically discreet from each other in a capitalist system, and to pass off the resultant confusion as a positive zone of emergence from which new innovative hybrids will emerge. I will also show how this can all be resolved by understanding the phenomenon of countertrade.

(*Quick note: by ‘crypto’ I am referring generically to a wide range of projects that specialise in selling crypto-tokens to the public for money (or in selling tokens for other tokens that can be sold for money). I am aware that there are nuanced differences between crypto platforms, but this piece is intended to provide a general model that can be adapted to different scenarios.)

The status quo formula vs. the crypto formula

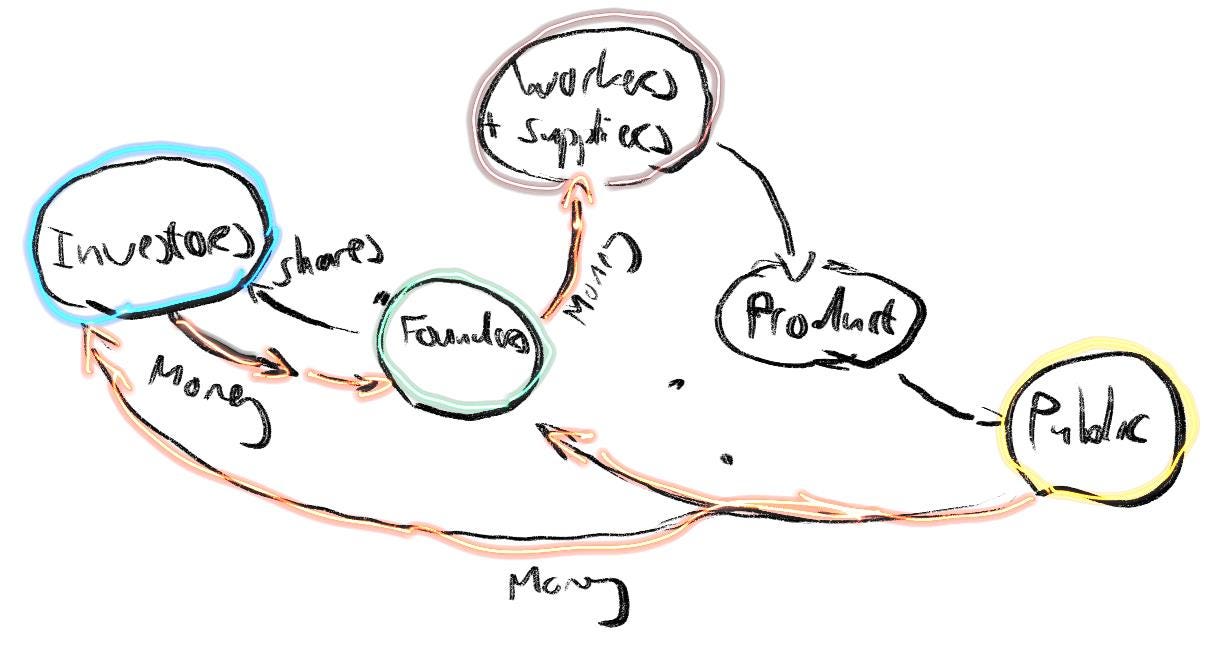

Many ordinary companies start off with a mismatch between their vision and their reality. If you launch a start-up, you might explain your vision to a group of venture capitalists, after which you might issue shares to raise money from them. The deal is simple: You give me money now to build out my vision, and I give you a legally enforceable contract that gives you a claim upon the future profits of the reality.

Once this is done, investors might sell their shares on a second-hand market, exploiting the fluctuating gap between the vision and the reality. The price of the share will change as investors guess how the product will turn out, whether customers will buy it, how much money will be earned in the process, and therefore how valuable it is to be holding a share that entitles them to a future cut.

There is a very low chance of category errors being made by the different players, because everyone knows what they are getting: the founders are getting money by giving the investors shares, and the public are getting a product. We do not find investors who believe that their shares are in fact the product or the money, and we do not find product buyers believing they have acquired money or shares.

There is little such clarity in the crypto world. The launch of a typical crypto enterprise looks roughly like the launch of a normal start-up. You start by explaining your vision, but rather than issuing legally-binding shares, you obtain money by selling ‘tokens’ to the public, but these tokens are often then characterised as the ‘money’ of a future platform being built. Rather than ending up with money in the hands of founders and a financial instrument in the hand of investors, we end up with money in the hands of the founders and… well... a sort of ‘future money’ in the hands of people who may or may not perceive themselves to be investors.

Furthermore, the token is – in many cases – presented as the product being developed. More often than not, I’m paying the founders dollars (or euros or pounds), so that they can hire developers and pay for marketing teams to build a platform that will turn my token into some kind of ‘money’. In my next Unboxing piece (available to Subscribers) I will be looking at a project does exactly this: they sell tokens to raise dollars to build out an infrastructure that is supposed to subsequently turn those tokens into a ‘regenerative crypto-currency’ to be used in a future ecologically sustainable society.

That’s but one example of this model, which has now been used countless times in the crypto world. The model causes all manner of confusion because it mixes previously discreet financial identities, but presents this as an innovation that will allow a person to fluctuate between different personas, as follows:

The Investor Persona: The token is seldom overtly presented as a financial instrument, and has no legal rights attached to it, but I buy it with money and I’m told that I can see myself as an ‘investor’. I’m also aware that the primary way I’m supposed to exit my investment is to resell the token to others for money. This is, at an experiential level at least, vaguely similar to how a shareholder experiences themselves, watching the price of a share go up and down, and deciding whether to hold on or to exit.

The Money-holder Persona: Unlike a shareholder, though, I’m simultaneously encouraged to experience the token as ‘money’ that I’m supposed to use for exchange. It’s a curious money, because it’s always quoted in terms of dollars (which the investor persona requires to make sense of it).

To me it is clear that these personas are antagonistic to each other, but I am told they can harmoniously co-exist. Typical narratives used by crypto promoters to explain how include:

Simply insisting that a movable token priced in money is the same as money. I can easily explain that it is in fact a countertrade object (see next section), but to crypto promoters the fact that the investment can be exchanged for things makes it ‘money’, because it is a ‘medium of exchange’ (see also How the ‘Functions of Money’ blind us to the Structure of Money)

Insisting that pricing is purely in your head, rather than an actual network phenomenon that transcends individual people. This is a complex topic, but the gist of it is that crypto promoters often say that the reason I use dollars to price things is not because the dollar system is a vast network vortex, but rather because I’m personally ‘choosing’ to see things in terms of dollars, and that I could also just choose to see the world in terms of this-or-that crypto token (this is a bit like arguing that national borders are imaginary, and that all I need to do to override them is to imagine a different border). This is how they then switch between the Investor Persona (who sees the tokens in terms of dollars), and the Money-holder Persona (who - apparently - sees everything in terms of the tokens)

More generally, there is an appeal to the unknown. When challenged about the tense stand-off between crypto tokens as investments and as ‘money’, the last resort is to insist that the crypto scene is in a transition period, that the technology is still young, and that there is some hitherto unknown hybrid form that will reveal itself in future. For a representative example of this line of reasoning, see this tweet from Bitcoin philosopher Troy Cross (he focusses on Bitcoin, but this could be applied to many different crypto tokens):

This vision of an emergent-yet-still-unknowable novel form is often pitted against any person who expresses any doubts about typical crypto narratives. It casts them as unimaginative, bound by convention, and ‘stuck in the old system’. But it is also true that someone who calls a spade a golden sword is likely to label someone who calls a spade a spade unimaginative.

In the tweet above, Troy complains that his favoured crypto-token is seen as ‘incoherent’, but crypto-tokens, like spades, are very coherent. What is incoherent is the golden sword brigade. And if there is one concept that the golden sword brigade really does not want to know about, it is countertrade, because it breaks the illusion of the apparent simultaneity of the investor persona and the money-holder persona. It does this by showing that an investor can use their investment for exchange, without that investment being money. I already did one whole piece on countertrade, but let’s go through it from a different angle.

Learning to see countertrade

Imagine an investor holding a share in a company, and that the share has a market price of $100. They can exit their investment by selling it to someone else for that amount. We can summarise it like this:

$100 dollars goes to the investor that is exiting

Share goes to the new investor

There is, however, another – unusual – way for them to exit: they could swap their share for something of equivalent price. Imagine their friend has a jacket that costs $100, and that they desire it. Rather than offering their friend money, the investor could offer a $100 share as compensation. If the friend agrees, a share will go one way, while a jacket will go the other way. It looks like this:

Jacket (costing $100) to the investor that is exiting

Share (costing $100) to the friend

This is an act of countertrade. Two non-monetary objects have been exchanged with each other, but only by using their monetary price ($100) to decide upon the exchange ratio. Countertrade is the act of abbreviating two offsetting monetary transactions into one seemingly non-monetary ‘barter’. To see this, consider the alternative scenario to the scene above:

The exiting investor could have sold their share for $100

And then given the $100 to their friend to buy the jacket

And then let their friend use the $100 to buy a share

They could have done that three-part process, but it is far simpler for them to collapse the three parts into one by just handing over the share for the jacket.

Swapping vs. buying

Normally we are easily able to recognise countertrade, and it turns up in our language in words like swap. In this scenario above, the investor is not going to say ‘I am buying a jacket with my share’. They will say ‘I swapped my share for a jacket’. They intuitively steer away from monetary language because they recognise that neither object used in the exchange was money, and that the money was rather a hidden force in the background.

Much of the category-bending and cognitive dissonance found in the crypto world results from the inability (or refusal) to recognise that this same phenomenon is occurring with crypto-tokens. If I take a crypto-token with a price of $100 and swap it for a jacket that costs $100, it is exactly the same process as I described above. What I should say is ‘I swapped a $100 crypto-token for a $100 jacket’. Implicitly, I am selling my token for $100, using the $100 to buy the jacket from my friend, and then letting my friend use the $100 to buy a token.

The actual money in this transaction is in the background. It is the $100, but it is invisibilised, because:

Countertrade in general makes money fade from sight

In the case of crypto countertrade in particular, one of the goods involved in the swap has the superficial appearance of money, so falsely gets credited for the role through its higher visibility than the actual money that has faded from sight

Let’s hone in on Point 2 above. Crypto-tokens are limited-edition branded digital objects with a price, but are very good at avoiding been recognised as countertrade objects, because:

They are almost always initially marketed as ‘money’, and are often coated in monetary branding, with monetary symbols and imagery of coins, and so on

They often appear as positive numbers on a screen, which is visually superficially similar to the numbers in a bank account (see my piece I-Token for a deep dive on this)

They have high movability, but low specificity: most countertrade is undertaken with slow-moving physical objects that have a clear non-monetary identity, and this makes the process highly visible. If I swap some obviously useful specific object (like a backpack), via its monetary price, with another obviously useful object, we immediately characterise it as ‘swapping’. It is also going to be hard for me to do that instantaneously across borders, because the backpack is a large physical object, so its countertradability (ability to be easily countertraded) is quite low. A digital token with a price, by contrast, has high countertradability (it can be countertraded rapidly with someone on the other side of the world), but it simultaneoulsy has no usefulness in itself, and no legal rights that would identify it as a financial contract. Given that it is covered in money-like branding, and that no other category of object will accept it, it will get shoehorned by default into the ‘money’ category, especially in situations where people already have a vague picture of the monetary system

This is how the tokens slip past of countertrade radar, and why a case of crypto countertrade ends up being described as an act of ‘buying’ rather than an act of swapping. This is how crypto promoters construct a vision of the tokens somehow competing against the monetary system, even though the tokens cannot be countertraded unless they have a price derived from the existing monetary system. This is extremely frustrating for anyone who can see through this, such as John Paul Koning, who vents his frustration here:

He points out, like I have many times before, that really crypto tokens compete against other money-priced investments (like shares, and so on), rather than the money used to price those investments. The only reason this is not recognised is due to the confusion caused by the high countertradability of crypto tokens relative to normal investments.

This is how we end up with the imagined simultaneity of the Investor Persona and Money-holder persona in crypto. We would all be better off if we recognised that the two real personas are actually the Investor Persona and the Investor-using-their-investment-for-countertrade Persona.

The ‘vision-makes-reality’ problem

Crypto promoters have one major advantage though. Their vague narratives can get past our bullshit radars by catching a ride on existing weaknesses in the public understanding of money. Much of my newsletter is dedicated to revealing those weaknesses, and helping people move past them. If you’ve been following this newsletter you should hopefully be able to identify the prevalent commodity orientation to money in our society (see, for example, Money through the eyes of Mowgli), in which people imagine money as some kind of movable ‘substance of value’, that in turn performs a series of vague functions. In its modern context, the commodity orientation results in people imagining money as a kind of ‘fictitious substance’ created through social agreement or belief, and this in turn leads to the idea that money can be created by getting enough people to believe (how many times have you heard someone say something along the lines of ‘money is just a belief system’).

It is this which gives crypto marketers a perfect opportunity to imagine that a countertrade object is on its way to ‘becoming money’, provided that more people start to believe in it. Start-ups often use a fake-it-until-you-make-it attitude, presenting a brave face to the public while they frantically scramble around in the background trying to turn their product into a reality. Crypto projects, on the other hand, often adopt a ‘faking-it-is-what-makes-it’ attitude, encouraging token-holders to put on a brave face and believe the system into reality.

Break away from the Cult of the Golden Sword

This would all just be so much easier if we called spades spades. Really what we have in the crypto ecosystem are thousands of sets of limited edition digital collectibles, often branded as money, but all sold for money, and traded on speculative markets for money. This is what gives them a monetary price, and the price is what gives them countertradability, which in turn allows them (in an ironic twist of fate) to be mistaken for money.

But isn’t it amazing what a spade can do? Just like the ability to dig holes is a useful capability, the ability for crypto-tokens to be quickly and easily countertraded across borders is an authentically useful property of crypto-tokens. There is no shame in being a countertrade object. In fact, I believe there is a new age of countertrade emerging (watch this space for a big piece on this). Indeed, the only people who refuse to see this are the Cult of the Golden Sword, but the future of spades should not be in their hands.

Great post. I've long been interested in using Ethereum to represent commercial real estate assets, an particularly to represent the cash flows they generate. In this model, a unit would represented as an NFT, and distributions/dividends would be linked to those units as transactions in dollar-denominated stablecoins.

Once you have enough assets on chain, and a history of distributions, it starts to look something akin to the stock market, where each stock has a history of earnings you can use to value it for trading. Importantly, that history of earnings is backed by enforceable legal mechanisms which rely on legal artifacts like 10-Q filings.

I still think this is a good use case and am working on a project to make it real. The challenge is that real estate investing is... pretty boring? Most real estate doesn't double or halve in value overnight. The relative lack of volatility is part of why real estate is such an attractive asset.

Trillions of dollars are locked up in real estate, but it's practically impossible to liquidate interest without selling the entire asset. Refinancing is an option in some cases but it's expensive and slow.

There's a lot of practical utility for this model, but it's not "when moon?" useful, so it's hard to get crypto bros to look at it seriously.

this was great!