An Emotional Guide to Fractional Reserve Banking

How our personal states of burnout are linked to bank overcommitment

Have you ever found yourself promising a friend that you’ll hang out, or telling your family that you’ll visit over the summer, or assuring your boss that you’ll get a big project completed in a couple weeks, only to discover that you feel extremely stressed when those committments actually get called in?

Believe it or not, this personal experience of overcommitment is a great entry point for understanding so-called ‘fractional reserve banking’. In this piece I’m going to explain why, and also show that the fractional reserve principle is used within many different systems beyond banking. Let’s start with fractional reserve relationships.

Fractional reserve relationships

Most of us run a fractional reserve relationship system. As we grow up we form relationships - with friends, family, lovers, associates, and colleagues - many of which require us to open ourselves up to being called upon by those who have expectations of us. Being entangled in such a social web means we commit to fulfil certain obligations that get called in at certain points by people, but it’s also how we get lines of support from others. Nevertheless, while you build these relationships over time, the obligations attached to them are not necessarily activated every day. You probably only tend to a small fraction of your overall commitments at any one particular point in time.

Put simply, the implicit promises you’ve issued out to the world exceed your ability to simultaneously handle them all at once.

Thus, imagine if two of your friends experience a crisis at the very same moment as your dad calls to ask you to finalise details of a visit you promised, just as your boss emails irritably asking for a progress update. You have a limited amount of emotional energy, but in the past issued a whole series of promises to people that are of greater magnitude than your ability to fulfil them simultaneously. But now they are being simultaneously activated, and are overrunning your emotional reserves. You find yourself trying to ‘juggle’ the calls upon your reserves: you pretend to not have seen your friend’s message, and ignore your dad’s call as you desperately try to buy time with your boss.

There’s no inherent problem with moderate overcommitment, and most people can manage it OK most of the time. After all, if you made no promises to others you’d probably have no friends, work contracts, or any ties to the world at all. Extreme overcommitment, however, gets toxic, and inspires quotes like ‘learn to say no’, or ‘it’s better to undercommit and overdeliver than to overcommit and underdeliver’, which encourage us to reduce the number of promises we issue out.

Excessive overcommitment can lead to burnout, but it’s easy to unknowingly enter into that state. A person who is burned out might have been buzzing and optimistic a year ago, and might have made a load of promises back then in the belief that they’d have the space and energy to cover them in future (they might have even made promises to themselves, such as ‘I vow to learn a new language in the coming year’). But once they reach a certain extent those promises (think of them as outward future projections into the world), start to extract far too much inner energy. Indeed, once you’re deep in a state of overcommittment, you find that everything starts to move sluggishly, because you can only deal with small fragments of the total committment at once.

In a situation of burnout, you may develop a phobia of people calling on you, because you feel overwhelmed by seemingly small tasks. A friend emails to say ‘hey, please check this over, it will only take 10 minutes’, but with so little emotional reserves, this small call can seem like a stressful ordeal. Overcommitting to potential things in future, in other words, leads to fear of actual commitment to actual people and things in the present.

So, what’s this got to do with banking?

Our small-scale personal overcommitment is like an emotional allegory for the large-scale system of money presided over by the banking sector. I’ve written various pieces showing that much of the money supply takes the form of bank IOUs - promises - issued out by banks. The banking sector issues these promises out far in excess of its ability to handle all of those being called in at once. But, while we may slide into a state of excessive overcommittment without being aware that we are doing it, bankers do it deliberately: overcommitting, and then managing the results, is at the deep core of banking. Before we get to that, however, let’s visit another fractional reserve system.

I wouldn’t be able to write this newsletter without the support of paying subscribers, so please consider getting a subscription! It’s only $75 a year.

The fractional reserve gym

Deliberately overcommitting sounds irresponsible, but for many businesses it makes sense. To understand why, let’s think about a gym. It’s a building with a finite floor space and a finite amount of equipment. Perhaps a particular gym has a maximum capacity of about 300 people, but if you are running this gym, should you only sell 300 memberships? You’ve got enough equipment and resources to ‘back’ the commitment you’re making: you’re promising 300 people access to the gym at any point, and you can certainly deliver it.

It would, however, be a major mistake to only sell 300 memberships. This is because not everyone comes into the gym every day, and not everyone comes in at the same time. Maybe only 15 of the 300 members come in at any one point during the day, which means the majority of your equipment stands unused. Your reserves are not called upon in full, and the vibe is going to be very quiet (we’re thinking pre-Covid times here).

Thus, if you’re the manager, you may think ‘if only 5% of members come in at any particular point, I can actually sell a lot more memberships and still cover the commitment’. Under the assumption that only 5% of members will come in, you can sell 6000 memberships for a gym with a 300-person capacity. You’re now running a fractional reserve gym. You cannot simultaneously serve all those people, but you’re assuming you won’t have to. Much like you might assume that only a small fraction of your friends will simultaneously call upon you for support, a gym owner is assuming that only a fraction of their members will come in simultaneously, and that the gym will have enough reserves to deal with that fraction.

The tradeoff now becomes apparent. With 6000 members, the gym’s reserves are going to be used to the full, and they’re going to be a lot more profitable, but if there’s a sudden small surge in the percentage of people coming in - let’s say it goes to 7% - they’ll suddenly have 420 people trying to get into a space that only holds 300. If that happens the owner will find themselves overwhelmed and under-delivering, turning people away at the door, emotionally exhausted by apologising. In fact, in that situation, the job of making excuses to those let down would become as draining as trying to serve those who managed to get into the gym.

It’s the business equivalent of burnout.

You can see a visual version of this article on Youtube here!

So, a prudent gym owner will certainly sell more than 300 memberships - to make sure that their reserves of equipment are made proper use of, and to make enough revenue - but will build in a buffer against dangerous levels of over-committment. Perhaps they will only sell 4500 memberships. Now, if there’s a sudden surge to 7% of members coming in, it equates to 315: there still might be some annoyed people at a busy time, but not nearly as much as before. The gym’s profits have gone down somewhat, but so too has the owner’s stress levels, and they are better prepared for variability.

The fractional reserve principle might be summarised as overcommitment in expectation of under-utilisation, and it’s a core feature of many systems that experience variable levels of use. It works most of the time, but can fall apart too. We’re seeing a very serious current example of its trade-offs in the health sector: most hospitals are only geared up to serve a fraction of society at any one point, which works most of the time, but when a global pandemic hits their reserves of bed space and equipment very quickly get overwhelmed.

Banking on overcommitment

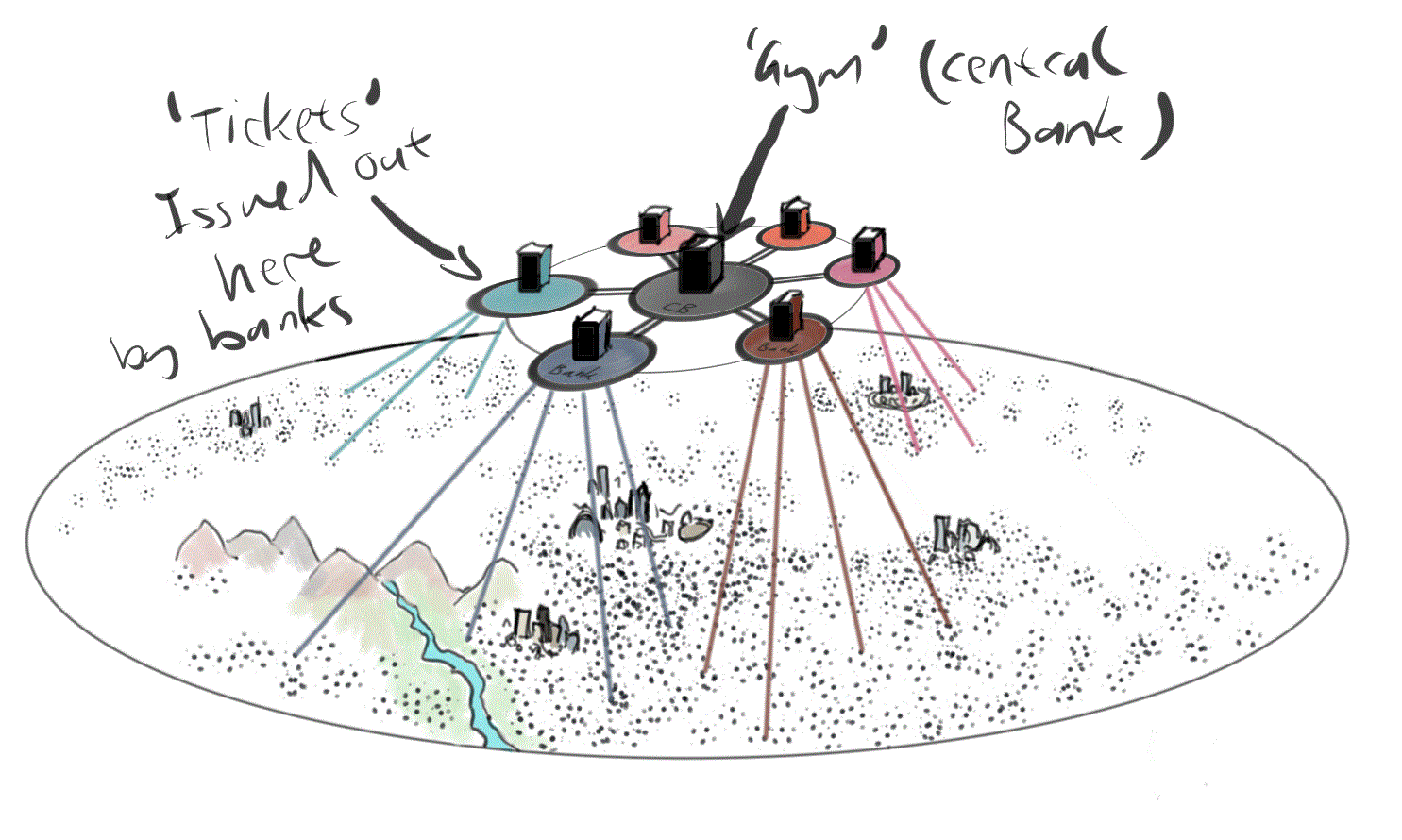

The biggest system of deliberate overcommitment in our society, however, lies within the banking sector. The units in your bank account are not state money. They are promises issued out by banks, promising you access to their reserves of state money (should you call upon them). Going to an ATM is an act of ‘calling in’ that promise. You are converting your digital bank promise into physical state money, somewhat like turning up at a gym with a ticket and demanding to convert it into entry. In the banking sector, the ‘tickets’ are the bank units you see in your account, but the actual ‘gym’ is the bank’s reserve account at the central bank.

Nevertheless, banks know that only a certain number of their account holders will ever redeem those promises at any one point. Indeed, most of our payments are not made by redeeming bank promises, but rather by reassigning those promises to someone else. The entire digital money payments system - which you interact with via your debit card, mobile app, or internet banking site - is built to facilitate the monetary equivalent of reassigning a ticket to someone else: it doesn’t - in principle - effect anything in the actual ‘gym’, but you might use it to resolve some private deal outside the gym between you and someone else.

Now, while an actual gym may sell memberships in excess of its capacity in order to harvest subscription fees, banks issue IOUs in excess of their state money reserves in order to harvest loan agreements. To briefly return to our emotional analogy, it’s somewhat like a machievellian ‘friend’ promising you a series of short-term favours to extract some much larger and longer-term committment from you in future, but one that is encoded in a contract that you sign.

This is referred to as ‘credit creation of money’, and it is called this because we see both state money and bank-promises-for-state-money as being ‘money’. I will do a separate piece on the details of that process (and check this out in the mean time) but for now let’s return to the gym metaphor and accept that the banking sector issues out far more ‘tickets’ than it collectively has in ‘gym’ floor space.

To nuance this, though, we need to alter the metaphor a little to move our focus beyond the situation of a single bank. Let’s imagine that the gym is the central bank, and that the individual banks are like private trainers who lease out different amounts of floor space, but who have the right to issue out tickets to the public on their own accord. They are collectively issuing out far more tickets than space, and to the public it looks like there’s a single class of tickets that floats around. In reality, though, those tickets are connected to particular trainers, and there’s an elaborate background process by which the individual trainers vie for floor space in the gym in response to movements of their tickets outside the gym.

If one trainer issues out tickets to their customers, but their customers then transfer them to people who are traditionally loyal to another trainer, you might find the latter trainer shouting at the former “give me some of your floor space so I can be prepared in case more people come in for me!” In banking terms, this is the process by which one bank demands that another bank transfers central bank reserves to them in response to the latter’s customers making transfers.

Imagine, however, that outside our ‘gym’ there is generally enough cross-flow of tickets moving between customers loyal to different trainers, such that the cross-flows cancel each other out, meaning the trainers end up with roughly stable floor-space. In the banking sector this is the process by which cross-flows of payments between customers of different banks cancel each other out. If you’re in the UK, for example, the various ‘multilateral net settlement’ systems (like BACS) are designed to superimpose the payments requests made between customers of different banks, and then cancel them out, such that only small amounts of central bank reserves (‘floor space’) move between banks while huge numbers of bank ‘tickets’ move between customers.

The result of this is that the banking sector as a whole can issue out far more promises than they have in reserves, but nevertheless expect the entire system to stay relatively stable, provided that the variation in the cross-flows stays within a certain band. And, if that doesn’t work out, the central bank can always step in, like a big boss-man landlord who owns the gym building, and who will have to take the hit if the trainers overpromise too much. This, though, is where my gym metaphor hits its limit, because a central bank - unlike our gym landlord - can expand the floor space at will. This is because our ‘floor space’ is state money, and state money is promises issued out by a state-backed central bank and treasury (if you want a different set of metaphors to get started on that concept, check out the last piece I did, about Ents and Squirrels).

Back to emotions

Let’s go full circle and bring this back to the example we began with. What is the personal emotional energy equivalent of the ‘gym’ with its ‘trainers’ issuing out excessive promises. At a personal level, within ourselves, we might imagine it as the different parts of our being making promises at different times: your professional persona makes promises to your boss, while your family persona and friend persona makes promises to family and friends. Maybe your romance persona promises affection to a lover, while your hero persona promises solidarity to global causes. On a day-to-day basis your emotional reserves get juggled as you give space to your various personas to fulfil the obligations they issued out. Ideally over time this simultaneously replenishes you with new emotional reserves, but when one too many things gets called in at once, you can hit burnout.

Unlike the banking sector, we don’t have a ‘central bank’ to expand our reserves of emotional energy to deal with such crises. Indeed, we normally have to take cover from burnout by drastically reducing our commitments and giving ourselves time and space to recharge. Indeed, when we excessively overcommit we tend to run down our reserves far faster than our ability to replenish them.

The banking sector doesn’t really suffer from this. The promises they issue through overcommittment boosts the money supply, and also leads the central bank into expanding their collective reserves. This process can go on for a long time, and lies at the core of capitalist systems.

In this you can also glimpse many of the mysteries of booms and busts. Much like we may exuberantly issue out claims upon our emotional energy when we’re feeling relaxed and optimistic, when times are good banks ‘reach forward’ into the future, or ‘lean in’ to the world, expanding their promises and pushing the wave of general optimism out into the world like a ripple of dominoes, as people spend while others hire. Indeed, when they expand their promises, banks can induce others to expand their promises too. You can imagine an unfolding across time and space, a rippling out of good vibes as everyone tells everyone that they can do everything.

But at some point that ripple outstrips the actual capacity of the earth and its people, and slows down. Somewhere far away it stops, and slowly starts reversing. Bankers might not see it for a while, but small cracks appear. Then suddenly the banking sector goes cold as they begin to imagine a wave returning to hit them, and they back away, or panic. They turn introverted, curling back from the future and from the world by retracting their promises. This is often when the ‘house of cards’ (or dominoes) can fall apart, and can lead to ordinary people rushing to ‘call in’ bank promises out of fear, rather than simply transferring them around. This feeds into more crises, and then the central bank must step in to counteract the curling in by issuing new money.

This is a somewhat rough assortment of metaphors, but hopefully a useful set. In case you don’t understand this, think about yourself. When you’re feeling optimistic, open and bouyant, do you reach for the future and expand your promises, or do you go inward and turn away? Probably the former. It’s only when you get burned that you curl away and generate fantasies of moving to a monastery somewhere to escape the commitments of the world. Have you ever had that feeling of ‘burning bridges’, that desire to just turn away from scenarios you can’t resolve rather than dealing with them? Well that’s the emotional equivalent of bankrupcy. You lose friends, but come out with a clean sheet to start over.

Not just a metaphor

If you emotionally overcommit, you deal with the fallout of underdelivering in the form of snarky comments from friends, rage from your boss and so on. If you’re a bank, though, you’re going bankrupt. You’re at the central bank requesting emergency injections of reserves, or you’re appealing to shareholders to inject reserves by buying new shares.

But while I’ve staged this piece as a series of comparitive metaphors, there’s actually a real world connection between large-scale bank overcommittment and small-scale emotional burnout experienced by individual people. What the banking sector (or corporate sector more generally) experiences as an exciting wave of ‘optimism’, is experienced by us at the human level as a wave of frenetic overwork. That’s because corporations only feel good when they’re standing to increase profits, whereas humans actually value many things beyond making profits. When making profits comes at the expense of family life, friends, connection to the wilderness, and connection to space and time, you feel burned out and miserable. You do not share the corporate exuberance, within which you may be but a small worker.

The opposite scenario of a corporate retraction burns people too. As banks and corporations become introverted, workers might get to slow down, but only at the expense of losing access to income, which for most people is mediated via the corporate sector (either directly or indirectly). And, because corporates don’t like the slow-down, they will attempt to extract more from their workers for less. Your co-workers get fired as you are expected to shoulder more burden for less pay.

It’s crazy to think that our emotional lives can be separated from the planetary scale economic structures that we are enmeshed within. To strive for holistic emotional balance, in which our emotional reserves are boosted not drained, we must seek to bring holistic balance to our economic system too. That’s a much larger topic for another time.

I much appreciate the unique exposition of "banking".

Thanks Brett. This reminds me of Joe Brewer's excellent piece 'The Pain You Feel is Capitalism Dying':

https://medium.com/@joe_brewer/the-pain-you-feel-is-capitalism-dying-5cdbe06a936c