Intro to Economic Life 7: Coming of Age in Corporate Capitalism

The phenomenology of life in market society

Dear free subscribers: The 10-part Intro to Economic Life course is for paid subscribers, but I’m opening this instalment up to everyone

In Part 5 we explored the fluid interdependence of a market system, and in Part 6 we looked into the worldviews that form in this context, such as commodity fetishism and the myth of independence. Nowadays it’s common for a person to go through an entire lifetime imagining that an economy is just a collection of individuals trading commodities, and that money is just a special - if somewhat mysterious - commodity that helps that happen.

Most of us are born immersed within a market society that will generate these worldviews by default, so it’s hard to get enough distance to form an alternative viewpoint. After all, it’s easier to see something if you can compare it to something different, and if you can’t, it’s often rendered invisible.

In Money as Addiction I showed how Zulu and Xhosa people in 19th century South Africa were forced into the market economy, and they very much could experience the jarring shift from tribal agro-pastoralism to capitalism, and could see the two worlds side-by-side. In some places this is still visible. To this day there are young Zulu and Xhosa people who return from urban employment to tribal homesteads where their grandparents might grow corn that gets ground into maize meal. Here are some Xhosa homesteads with subsistence agriculture patches.

Even my grandparents in Zimbabwe would grow some of their own food, and live within a type of hybrid ‘syncretic’ capitalism (see Part 4). My grandfather was a vehicle dealer selling auto-mobiles produced by distant corporations, next to a gas station that sold fuel from oil refineries, but his dusty town of Masvingo was full of informal markets, strong community reciprocity and subsistence agriculture.

As the scale and intensity of capitalism has increased over time, however, the amount of space outside the market vortex has diminished as ever more areas get sucked in. This is what we call commodification.

In many parts of the world, new generations are now growing up almost fully immersed in corporate capitalism, a market structure dominated by inescapable mega-firms that constantly seek out new frontiers of commodification. Twenty years ago we’d struggle to conceptualize food outside a supermarket, but now we have kids who struggle to conceptualize navigation outside of Google, communication outside of WhatsApp, or dating outside of apps.

Not only are new areas - like dating - constantly sucked in, but the older frontlines of capitalism become the ‘outside’ to the newer ones. In 19th century South Africa, tribal people were forced to pay tax in physical notes and coins, which were the cutting edge of the monetary economy at that time, but nowadays digital payments giants like Visa spearhead an all-out assault on physical cash. Older capitalism allowed payment without intermediation, but - in the current moment - that’s perceived as slowing down the vortex. Newer automated surveillance capitalism requires digital payments, and this manifests in the cultural realm as an ideology that says cash is ‘inefficient’ or ‘inconvenient’. Kids are now being born into that ideology, which means they could well become adults without awareness that there was once an outside to Big Fintech.

As the outside space gets eaten up, we find it increasingly hard to find those contrasts that might have once highlighted the inner dynamics of our system. Each new territory claimed creates a new state of mental capture, but this is justified - and even celebrated - by using ‘solutionist’ progress narratives that present growth and acceleration as an ever-increasing ‘high score’ for our civilization.

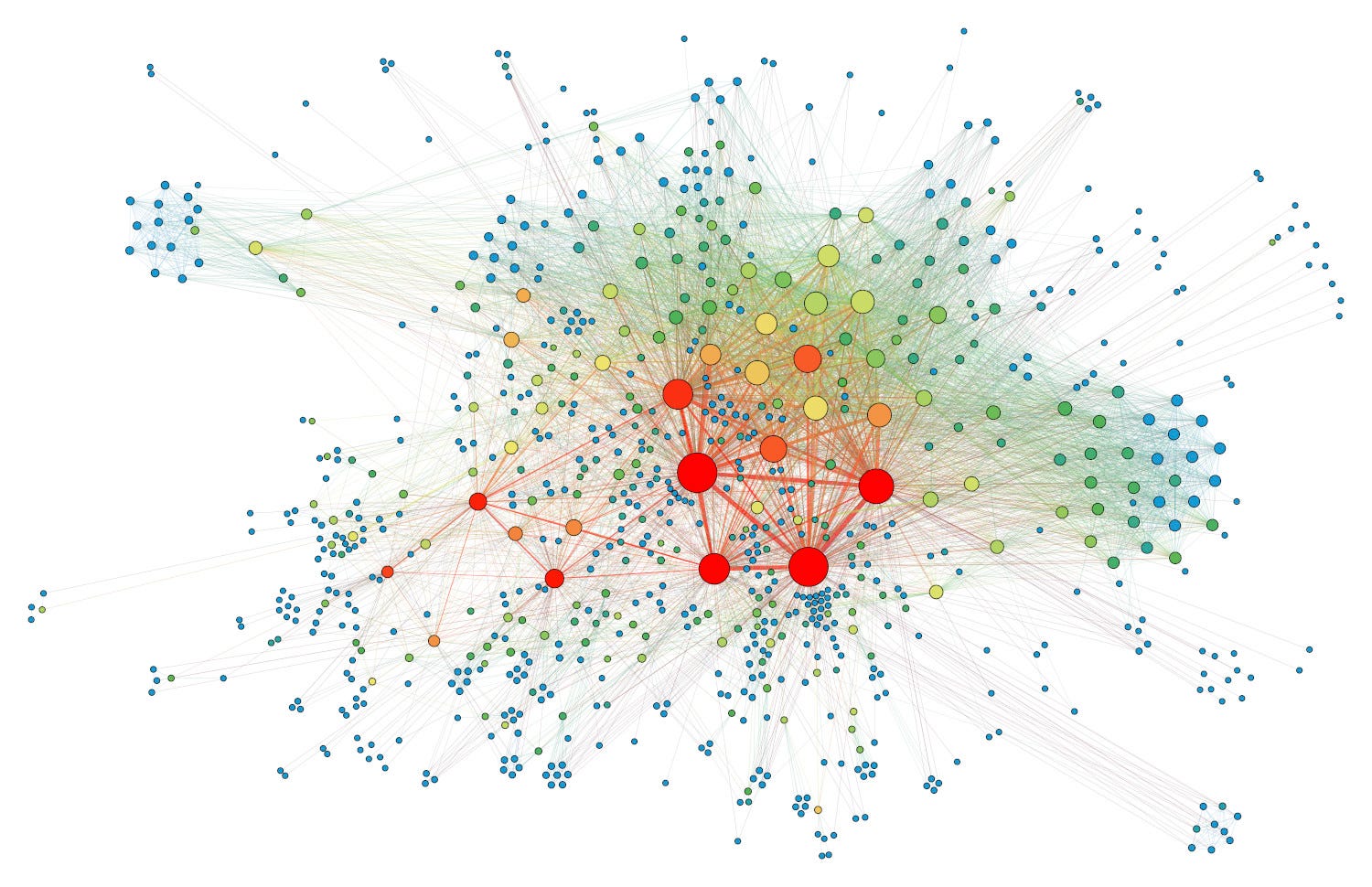

One thing that’s obvious, though, is that this ‘high score’ is achieved by making us ever more dependent on oligopolies of mega-players. In Part 6 we started exploring how power in a market network begins to concentrate into an oligopoly of big players. Picture the big red nodes below as corporate ‘titans of industry’ that have entrenched themselves into the centre of our economic network.

Almost every industry in the world is dominated by a small handful of firms (often no more than 10-20, and sometimes even less), but how do these titans get so big? Well, there’s a range of systemic processes in a market vortex that will do this. For example:

Asset accumulation: We explored this in greater depth in Part 6. The more money a firm has, the greater its ability to command workers to build new assets, and then command workers to run those assets to build more stuff. Over time, this culminates in corporate domination over the ‘means of production’. This leads to a hierarchy, not only between business owners and workers, but between larger businesses and smaller ones in different industries. For example, to survive nowadays, a small printing business must submit themselves to Google Maps, and must tether themselves into Visa and the banking sector. To use our ‘input-output’ language from Part 5 and 6, those mega-firms have entrenched themselves as inputs to everyone else, thereby becoming inescapable infrastructure

Power over suppliers: As mega-firms accumulate assets, it increases their market power and their ability to dominate over their suppliers e.g. if there’s one massive supermarket that dominates in a country, then a small salt producer trying to sell from the shelves can be forced to lower their cut of the final price. This can help the big player outcompete smaller supermarkets

Economies of scale: A fixed asset is something that can be used multiple times, and it might be required by a business to compete, but some fixed assets only make sense when used at large-scale. To use an extreme example, it’s incredibly expensive for a home baker to get an industrial dough mixer, because it will be massively underutilised relative to how much bread they make, whereas a big commercial bakery will find that input a lot less expensive relative to the amount of bread they’re outputting. This is one example of an ‘economy of scale’. In essence, bigger businesses often experience their fixed assets as cheaper

Mental capture: Large players entrench themselves in our minds through the ubiquity of their marketing, but also simply due to their constant presence in our environment. Their products are visible everywhere, their logos are in every high street, and their announcements get freely reported on as front page ‘news’ (something that small businesses would have to pay dearly for)

Inertia harvesting: Many of our so-called ‘choices’ in a market system are just inertia. A tired person walking home after work just drifts into the first supermarket they see to grab the first box of cereal off the shelf. The more presence an entity has, the more of that drift it captures. In the UK, for example, supermarkets like Tesco and Sainsbury’s are like giant drag-nets that capture money from the passing public

Lock-in: In the digital era, the longer you use a platform the less able you are to leave it. For example, you theoretically could choose to leave Spotify, but if it has accumulated a decade’s worth of data on you, and hosts all your playlists, the cost of leaving it is very high. Social media platforms like X now have a zombie-like feeling precisely because large numbers of people want to leave but feel they can’t (this lock-in is what Yanis Varoufakis calls ‘techno-feudalism’)

Symbiosis with states: Major firms can use their size to extract concessions from governments, and alter regulations through lobbying. The ‘revolving doors’ between industry and politics are extensive (e.g. former UK prime minister Tony Blair consults for J.P Morgan, while former deputy prime minister Nick Clegg works for Meta)

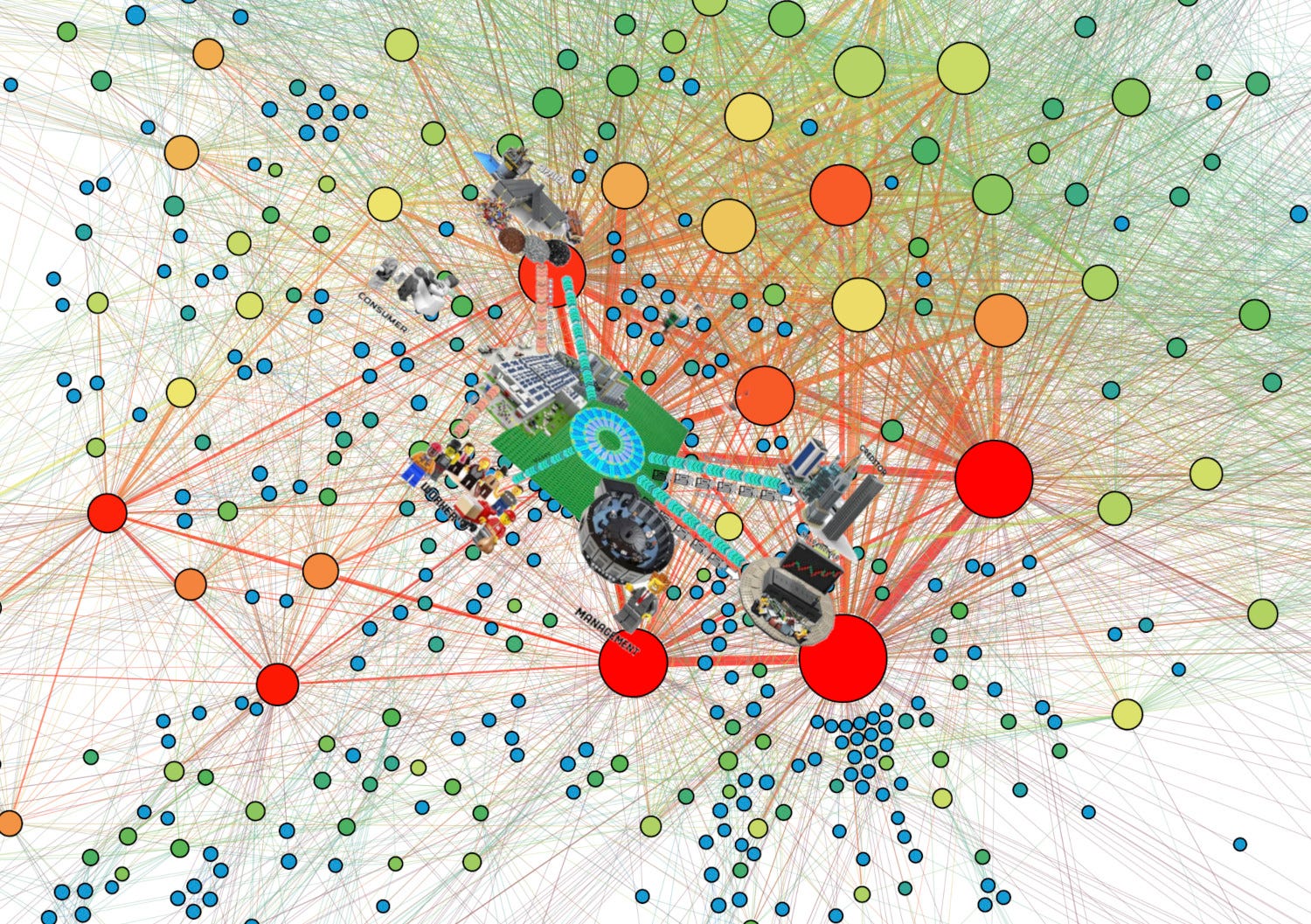

Symbiosis with Big Finance: Rich people help other rich people by contributing to the financing of their new projects in exchange for a cut of the profits (see my Lego Model of Financial Capitalism). More generally, large players have priority access to the financial markets, and can secure financing on much better terms than smaller players. This boosts their asset accumulation ability. This is what I was visualizing in my Lego Model of Corporate Capitalism, where I show the financial sector taking the lead on ‘charging up’ international corporations, which then blast out that money to mobilize workers and suppliers to produce stuff, which eventually manifests on shelves in front of you…

The image above is a corporate ‘circuit’, showing the different players who come together under a corporation, but how does this fit into the bigger picture we saw earlier? Well, the corporate entity above would be but a single sub-system in our overall system. Let’s visualize this by superimposing the two images:

Most people don’t think about economies as being tangled mesh structures like this. After all, if you’re just a tiny node in this system, it’s like being subsumed within a vast maze where all you can see is the immediate surface in front of you. More specifically, you’ll be surrounded by interfaces.

The Surfaces of Corporate Capitalism

What do I mean by this? At a philosophical level, an interface is any outward-facing surface of a system that you’re supposed to interact with. For example, you’re supposed to look at the window displays of Westfield Mall, but you’re not supposed to creep into the alleyway behind it to watch a loading bay worker smoke a quick cigarette by the dumpsters crammed full of empty boxes. You’re supposed to look at the advert for a diamond necklace in Kuala Lumpur, but not supposed to investigate the mining compound of De Beers in Namibia. You’re supposed to look at the menus on your iPhone screen, but not the international system of fibre-optic cables and datacentres that it connects into. You’re supposed to drift through the shelves of Tesco without thinking about the complex supply chains, and you’re supposed to plug your kettle into the electrical socket without thinking about the militaristic states that support energy giants. You’re supposed to look at the price charts on a Robinhood trading app without thinking about the hundreds of thousands of labourers that extract the things that will lead to the profits that will manifest as a slight change in a share price.

All of these things (display windows, touchscreens, supermarket shelves, plug points, apps etc), are interfaces that enable us to touch systems we don’t understand. Interfaces reduce complexity while increasing the obscurity of all those ‘behind the scenes’ schematics of a system, which are pushed into the background as irrelevant. So, as a tiny toddler stumbles down the street, they’ll be bumping up against different interfaces of our colossal economic infrastructure and the giants within it. As they touch things in shops, see their parents open wallets, and blink at the bright lights of billboards, their neural circuits are being calibrated by the corporate capitalist environment. They’ll grow up to see it as normal and universal, even if it’s only existed for a couple hundred years out of the 200,000 years of human history.

Our toddler’s conception of ‘the economy’, then, will be built from a mash-up of disconnected fragments. Here’s some things they’ll encounter:

Strangers: lots of people they don’t know walking past them, or drifting through stores, or standing behind counters. These people don’t seem to know each other either, but still somehow interact

Product displays: objects arranged on shelves, or on Amazon.com pages, or on the screen of their parent’s phone

Prices: little numbers with symbols next to them that accompany all products

Money: a mysterious object that seems to have the power to command people to hand things over, or turn up at your door with a food delivery. It might appear as a banknote, or a card or phone touched to a terminal, or a click on a screen

Firms: they’ll see lots of bright signs, logos and brands that repeat themselves along high streets. They’ll learn that certain products are associated with certain named entities

Corporate personhood: they’ll hear people speak about these entities as if they were conscious beings. Their dad tells a friend that “We’re flying with Emirates”, rather than saying “a pilot and crew is going to burn fossilized carbon to make a big machine, made by other people, fly”

Marketing: these entities saturate the environment with a form of culturally acceptable chronic lying. The firms always interrupt proceedings to make inauthentic and irrelevant associations between non-market things - like friendship, family, adventure and love - and particular products

Jobs: our toddler will be aware that their parents leave to ‘go to work’ at these entities, and over time will realise that they do so to get the money required to get the goods from the strangers. They’ll be asked ‘what do you want to be when you grow up?’ This eventually turns into anxiety about the need to find a limited slot for themselves - a job - hidden somewhere in the sea of strangers and products

Class, and status symbols: they’ll become aware that certain people do certain jobs, and that there’s different status attached to these. They’ll recognize broad ‘classes’ of people split by their level of economic power. High status is associated with rich people, entrepreneurship, and luxury products

Hierarchies and inequalities: they’ll notice that the richer people boss others who are more submissive. These bosses are culturally favoured, and the really big bosses have their faces on the pages of magazines, and get asked questions about the world on shows, as if they were sages. They apparently ‘built’ the companies that ‘create jobs’ for the submissive people

The state and taxes: our toddler will see police vehicles that patrol around the high streets to protect property. Over time they’ll form awareness that their parents have periodic obligations to hand money to the state, but - having made the earlier association that goods only come after their parents earn money - they’ll imagine that the state collects taxes so that it too can pay for things. This metaphor of the state as a household will coexist uneasily alongside their awareness that the money handed to the state comes branded with symbols of state power. There’s no immediate way to reconcile those disparate observations, so they’ll probably just separate them into ring-fenced compartments in their mind to deal with the cognitive dissonance

The financial sector: The feeling of large-scale bureaucracy isn’t limited to the state. Our kid will also experience it as they stand in line with their mother at a bank, or watch their dad opening an account statement for his investments. They’ll form a distant awareness of the financial sector not only as a realm of money, but of abstract forms, numbers and graphs

All of this will form a hazy mish-mash. Bills sitting in the post tray while dad complains about his boss, checking investment tips on Reddit forums. The beeping sound of a contactless card terminal with an ApplePay sticker on it that preceded the little toy they now play with, with its polyester tage that says ‘Made in China’. Our kid’s brain will slowly cluster these fragments into discrete realms, each with its own native logic: Their parents are employees when they’re away at the office - or when they’re trying to have a professional Zoom call at home - but they’re consumers in a shop, a taxpayer relative to the state, and a saver relative to the financial sector. They’re not whole beings in a multidimensional mesh. They’re split into these separate personas.

Mastering the Interfaces

As a little kid holds their parent’s hand on a high street, the people passing by will look like random atoms. Rather than seeing the complex webs of interdependency, they’re going to see solo agents bouncing off each other chaotically.

The kid will feel alienated by this sea of atoms, but will cling onto the protection offered by a background ‘molecule’ that they’re part of. Their families and friends are the protective cluster that holds them in place amidst the strangers. Picture our kid as the orange atom below, standing behind their mother (the yellow atom) at a pharmacy while she interacts with another seemingly ‘independent’ individual behind the counter.

Each person has some arrangement of protective connections that surround them, and this ‘molecule’ will condition their expectations of their (future) role. To this day, the Seven Up! series stands out as one of the most brilliant studies of how economic aspirations are built in different social classes, and how they play out over a person’s lifetime. The series took twenty 7-year olds from radically different backgrounds in the UK in 1964 and interviewed them about their views and goals, and then repeated this every seven years until they were in their fifties. Below you can find the opening episode. I recommend watching the entire series (it’s all on YouTube), but jump to 33:15 if you want to see how the kids’ perception of their future role has been affected by their family ‘molecule’ (or lack thereof - two of the kids are in a children’s home).

These perceptions held by the kids do not fully come from ‘inside’ them. They were projected from the outside via instruction, example, and interpellation (the process whereby authorities, parents and peers reverse-engineer beliefs into you through leading statements like “which university will you attend when you grow up?”) This process is ongoing. For example, middle-class teenagers will condition each other through rumours and advice like ‘You should get an internship at a bank’, ‘You have to post your fashion designs to Instagram’ or, ‘you’re screwed if you don’t master AI’.

In Part 4 we looked at Hadza hunter-gatherers, who historically have found it easy to decide upon their future role. They’ll join the others hunting. People in tribal society often get inducted into roles through rites of passage that give them secure access. Teenagers in a market society, however, face existential anxiety. They’re not only getting directives from corporations to buy particular products or else face social exclusion, but they’re being told to find that mysterious job to seek ‘independence’. What this really means is that they must step out into that confusing mass of people and things, in order to compete to find, and protect, a small slot for themself within the interdependent network.

They’ll be told to ‘make connections’, which is the process whereby you try to identify some basic clusters of interdependence within the seemingly random atoms.

‘Working class’ jobs often operate in short cycles and have a more immediate impact, like a person sewing buttons onto a quota of shirts before clocking off, and then repeating it the next day. People pushed into these roles often form horizontal solidarity systems. For example, Berlin’s gig economy bike delivery services have many South Asian workers, who undoubtedly introduce newly immigrated friends to the depot managers (here’s a whole academic study about that).

Third generation Turkish immigrant teenagers in Berlin, by contrast, might be pushed into a family-run bakery when they’re 18, and might be the manager with two kids by the time they’re 28. Their speed of ‘growing up’ is affected by their economic position. German teenagers with richer parents might never consider working in a bakery, and they have a financial buffer, so might be in their late 20s before they commit to a path in start-up culture, big business, NGOs, the arts, or journalism. Even if they have a set path - like a German 20-something trying to climb the ladder at Commerzbank - they might be 35 by the time they’ve built the required skills and connections to progress to middle management. They might delay having kids as they try to master their elite position, with its longer training and bigger deals and ongoing management of whole sections of a company rather than piecemeal work.

The classic UK sitcom Only Fools and Horses followed the lives of working-class Londoners striving to move up the economic ladder by resorting to wheeler-dealer scams and schemes. The hapless protagonist Del Boy is constantly on the lookout for ways to ‘make a quick buck’ by selling knocked-off watches or masquerading as a chandelier renovator to the super-rich.

The series is a treasure trove of class politics, but also highlights shifting class aspirations. Del and his younger half-brother Rodney are constantly hampered by their lack of ‘social capital’ - connections into the culture, norms and solidarity networks of the rich. In one episode, there’s a heartfelt scene where Del gives up a big opportunity out of loyalty with Rodney, who he’s tutored in the ways of the black market. If Rodney were to have kids, however, he may try to push them to seek jobs in big conventional corporations. Without parents with social capital, however, they might be forced to rely on the business self-help books at a second-hand bookstore, like these ones:

Look at the titles. To Sell is Human. The Google Résumé. Creativity, INC. The Seven Spiritual Laws of Success. The Innovator’s Dilemma. Self-help culture is characterized by a few key things. Firstly, it presents the economy as if it were some natural storm that you must master. You don’t need to understand what drives the storm - it’s simply taken as a given - but you are told that success is all about riding the waves it generates. It also individualizes and depoliticizes this act of riding: the overarching vibe is ‘life’s unfair, so get used to it, stop whinging and take personal control’. Self-help culture is central within conservative libertarianism, the political ideology that we touched upon in Part 6 (see also, Detachment Theory).

Libertarian self-help culture pushes you to fixate on the surface of capitalism, rather than the deep structure. That may sound like a critique, but I say this with a degree of empathy. While libertarianism can be deployed by economic elites as a kind of smoke-screen to disguise power in the ‘storm’ (like an aristocrat telling Rodney that he simply needs to ‘work harder’ to move up in the world), it’s also a narrative that offers some (often illusory) comfort to an alienated person in a vast system. The message is: if you can’t change the system, change yourself.

Exercise: Surfing storm swells vs. understanding them

Self-help culture can be useful, but it deliberately ignores deep processes. For example, here’s a short surfing self-help video:

This video will help you surf, but it would be tough to try to derive an understanding of oceanic physics from it. Similarly, self-help business books can teach you to write a CV, or design a business plan, or identify a product niche, but they’re not designed to explain the underlying ‘physics’ of capitalism. Now watch this one…

This video goes deeper into oceanic physics. In our business metaphor, this might approximate the training you might get in an MBA program. It still skirts over the deeper complexity though. For example, it doesn’t explain why the wind blows across the water, which would require you to look into atmospheric science and solar radiation. It also has a very limited focus and goal, which is to explain surfing. Much like surfers see no practical need in understanding how the nuclear fusion in the sun affects winds that affect the ocean, entrepreneurs see little point in understanding how the dense interdependent economic mesh, with all its class dynamics and concentrations of power, manifests as economic waves they can try ride. So, how would go about designing a course for surfers that de-centres them from the picture, and enables them to contextualize themselves within a much larger system? Feel free to post suggestions in the comments.

The Five Vibes of Economics

Let’s imagine that Rodney’s child is a more sensitive sort, who prefers to understand how things work rather than being an entrepreneur. How will they go about understanding the deeper ‘physics’ of capitalism? Well, they’d see economists on the TV explaining the economy through formulas, theories and numerical statistics, as if economic life was indeed akin to particle physics. This would clash with phenomenology - the lived experience of what it feels like to be in an economy - but it would certainly claim to offer some scientific objectivity.

Modern Economics has been around for a couple hundred years now, so it’s not a uniform discipline, but it does have certain quirks - or perhaps fatal flaws - embedded into its foundations that give it a particular vibe. For example, mainstream Economics leaves out actual physics - like the laws of thermodynamics - from its ‘scientific’ analysis of economies. An economics textbook never starts with a reflection on how the sun powers our bodies through the food we eat, and powers our machines through the stored energy of fossil fuels.

Rather, the ‘physics’ described in a standard Economics 101 textbook are the physics of the surface appearance of capitalism. The basic Econ 101 move is to accept our market worldview (see Part 6) at face value, which is why they always start with individual beings who produce things, and who are then imagined to enter into exchange as a voluntary act. This relies upon a background imagination of the economy as a disconnected series of individuals that do deals, but - as we saw in Part 6 - that’s an illusion generated by default in a situation of large-scale fluid interdependence. Market society forms scales over our eyes that filter out awareness of interdependence, and which render everything in commodity terms. From this starting point, a microeconomist then might claim to have some insight into a shadow-world of rational calculation calling the shots in our life, and yet that’s what you’d expect an alienated person under large-scale capitalism to imagine.

In many ways then, conventional Economics is just an accentuation of the native cosmology of capitalism. It takes those scales over our eyes, and formalizes them into goggles with lenses adjusted for purity. Economists might have intense debates as to what adjustments to make, much like theologians bicker around the outside of a central point of faith, but they share basic background tenets. This is what Rodney’s teenage child will learn if they go into the second-hand book store and - like me - pick up a copy of Microeconomics (Fourth Edition), by Robert S. Pindyck and Daniel L. Rubinfeld. Here’s the first page of my copy:

It seems innocuous enough, but what are these ‘units’ they speak of? The units are supposedly discrete individual actors of different sizes who make independent decisions. These decisions supposedly culminate in the broad phenomena that macroeconomics then studies. Our textbook hints at a larger interdependent structure when they note that an individual or entity might play ‘a role in the functioning of our economy’, but they imply that the structure is the voluntary creation of individuals. Put differently, independent individuals are seen as logically prior to entangled interdependent networks. This is a bias referred to as methodological individualism.

Let’s pinpoint some of the basic vibes that emerge from this starting point, which get passed on to students:

Vibe 1: Emphasis on individuals: Economics starts with a vision of ‘independent’ adulthood (what our microeconomics textbook calls a ‘unit’). In the first instance this is a fully grown adult, but it becomes a metaphor for larger ‘units’ like firms, industries or states. Economists then try to model how they bounce off each other

Vibe 2: Emphasis on rational calculation: To do this modelling, economists must give these units a particular character. Initially, this was Homo Economicus (see Part 2), with the units being see as calculating, self-interested, utility-maximising entities. Over the years this has been altered (e.g. Daniel Kahneman’s work in behavioural economics made the units more ‘irrational’), but Homo Economicus is like a ghost that continues to haunt the discipline

Vibe 3: Emphasis on choices: Our textbook above fixates on the choices and decisions made by the units. This might be people choosing what job to do, or what product to buy, or a firm deciding what to invest in. The fixation upon this (allegedly) voluntary choice is based on another shadow thought-structure, which is the myth of exit. Note how they present workers as having some open-ended ability to choose ‘where to work and how much work to do’. It’s almost as if they imagine that workers could choose to not work, as if we all had the option to just walk away from society, to back out of the structure and dissolve the relations

Vibe 4: Emphasis on exchange: Economics de facto assumes that our primary ‘economic decisions’ take the form of exchange. Put differently, they seldom recognize any moral logic beyond formal tit-for-tat reciprocity, and don’t take seriously David Graeber’s perspective that we covered in Part 3. Any moral logic beyond exchange is either seen as outside of economics, or explainable by exchange

Vibe 5: Emphasis on equilibrium: if your starting point is solo individuals who are temporarily driven by choice (and by a particular motivation) towards each other to exchange, you need a resolution point that will cause them to retreat back to a point of stability, having all been satisfied. This imagined stable state of resolution is called equilibrium

There are various other vibes that can be derived from these ones. For example, economists will often also have:

Commodity orientations to money: if your worldview starts with floating people trying to convince each other to exchange floating commodities, you will probably also by default generate a mythology of money as a special floating commodity with a special power to induce people into action. Many economists know that money actually isn’t actually a commodity, but will nevertheless use this metaphorical framework to treat it as if it were, because their underlying paradigm starts to tremble if they don’t

Everything as calculated exchange: as we saw in Part 6, markets and exchange are just the ‘tip of the economic iceberg’, but - in the hands of economists - that tip often gets used to explain the base of the iceberg. This is not restricted to economists (for example, classical liberalism explains society as a contractual deal between individuals) but economists have a track record of pushing this logic to an extreme

Depolitization: a worldview made up of solo units voluntarily trading is politically useful if you want to disguise power relations. Big banks, for example, would never use standard economics for their trading decisions, because they know that markets are driven by power and herd behaviour, but it’s politically useful for them that economists present markets as if they were driven by apolitical physics (see my entry on euphemistic libertarianism in Detachment Theory)

Object and nouns, rather than processes and verbs: This is a complex topic, but Economics often has a mechanical or ‘dead’ vibe to it, as opposed to a morphing organic vibe. That’s because, deep in the recesses of their minds, economists often picture our underlying reality as stable objects - e.g. self-contained people and things that can be labelled through nouns. These then go through moments of instability (e.g. exchange) before reaching equilibrium again. This is in contrast to worldviews that see our underlying reality as unstable change characterized by endless active processes that can only be labelled through verbs. In the world of process philosophy, for example, the apparently stable objects that economists model are actually just illusions that form at the intersection of processes

Rewiring our economic metaphors

Many economists would protest at the account I’ve given above, and strive to show that they’re more nuanced. And certainly, most of them are more nuanced in their particular sub-fields. Nevertheless, these vibes constantly rise up out of the discipline like zombies that get re-spawned no matter how much you try to fight them. This is easily witnessed when you encounter the most politicized versions of the underlying paradigm (e.g. like a free-market conservative TV commentator, or a start-up founder who believes they’re ‘self-made’, or a Bitcoin promoter who believes that state money is a ‘fake commodity’ to be contrasted with true money, which should be an apolitical commodity that facilitates exchange between solo individuals).

At some deep level, Economics just has the direction of its primary metaphors wrong. If you had to isolate one of your cells from your body, it would quickly die. This means you cannot start an analysis of your body from the assumption of solo cells, precisely because that’s a point of death, not life. Much of Economics has a background model in which solo cells - units - voluntarily ‘decide’ to form interconnected tissue, but this is a fundamentally flawed starting point, like trying to imagine living cells existing outside of muscle tissue.

In reality, choice is a relatively shallow surface phenomenon. We begin as interconnected tissue, and later, if you’ve built the strength and skills, you can temporarily rip yourself out of that to reconfigure relations, like a cell pulling away from one tissue to re-graft onto another. That’s like you changing jobs: you have a brief window where you can survive without being part of some ‘tissue’, but you have no fundamental reality in which you could remain adrift.

Let’s shift back to our earlier metaphor. Children know that they are not ‘independent’ as they cling to their ‘molecule’, but they begin to forget it during their individuation process as they shift towards reliance on the fluid interdependence of monetary markets. There is no such thing as true ‘independence’, but they certainly will create a folk story in their head about being independent. This is what Economics formalizes, and this is why Economics is so ill-equipped to explain the world.

It’s important, though, to have some empathy for economists like our Robert S. Pindyck and Daniel L. Rubinfeld. They too were once little toddlers experiencing the chaotic world, and at some point they entered a university and found a worldview that helped them make superficial sense of that. They would have started to apply that to their experience of being in a supermarket, or filling out a job application hoping to win a position at the university faculty. To win that position they’d have to show proficiency in that same paradigm, and show how they could use the ‘tip of the iceberg to explain the base’. This is how economists end up working to reinforce our illusion of separation with an academic field. Once they’re entrenched as professors, their livelihood depends on them maintaining that myth.

If you’re truly interested in describing capitalism, rather than its surface layer, you have to start with entangled collectives in a state of dynamic and involuntary enmeshment. After that you can begin to think about secondary phenomena like ‘individual choice’. Equilibrium is a passing phenomenon at best, because even if you close a particular transaction in the market, you’re not retreating to fundamental stability. You’re retreating into some other form of dynamic interdependence, like everyday communism or informal reciprocity and care networks. You’ve never been in some solo state, and equilibrium - a state of fundamental rest - only occurs when you die (and even then you get absorbed into other processes). We are constituted by others, by ecologies, and by the sun, without which we simply do not exist.

Coming up next…

In the next instalment, we’ll explore how our fragmented worldview, experience and state of lock-in prevents us from seeing the problems of our economic system, or from feeling them when we do see them, or from doing anything about them when we do feel them.

These essays are very well done: clear and well thought out. Really remarkable. Thank you!

Orthodox (or if you prefer mainstream) economics isn't very useful because its assumptions are rooted in ignorance of both human biology and anthropology.

And this fundamental set of errors is compounded by the backgrounds of the sort of people who choose to work in the field -- there's a surfeit of math and physics and a dearth of biology. It's simply a fatal combination for a project which aims to predict and/or organize human group behaviour.