Dear Reader. This is one of those slightly geeky pieces that I do occasionally for the curious non-expert. For those of you who aren’t into my more technical stuff, you can find my more social-political-cultural work in sections like Big Techtonics and Winging It.

In this piece I’m going to wade into Modern Monetary Theory (MMT) again - building on my MMT primer video from last year, and the follow-up piece Levelling up my MMT (Part 1). In this piece I’m going to build out my own idiosyncratic way to approach the theory via 10 steps.

I don’t characterise myself as an MMT campaigner, but I do feel an affinity towards the broad paradigm behind it. That’s probably because I come from an anthropology background, and anthropology has a similar historical battle going on with mainstream economics.

In short, mainstream economics metaphorically speaks of money as a commodity, and does so for ideological reasons (see, for example, The Archipelago), whereas both MMT and anthropology are much more attuned to seeing money as a system of credit, with IOUs or promissory instruments (which may or may not be hosted in commodity bodies). If you want to delve a little into the background battle around that, check out 5D Money and The Anthropologist in an Economist World.

Given that much of my work is public-facing, and intended to try bring in non-experts, I enjoy doing stylisations, simplified and abstracted but useful portraits that can give a person neural scaffolding so that they can go and complexify the issue for themselves at a later date. So, I’m going to lay out 10 stylised sketches of different concepts below. Don’t see them as perfectly accurate. See them as components that you can modify and recombine for yourselves.

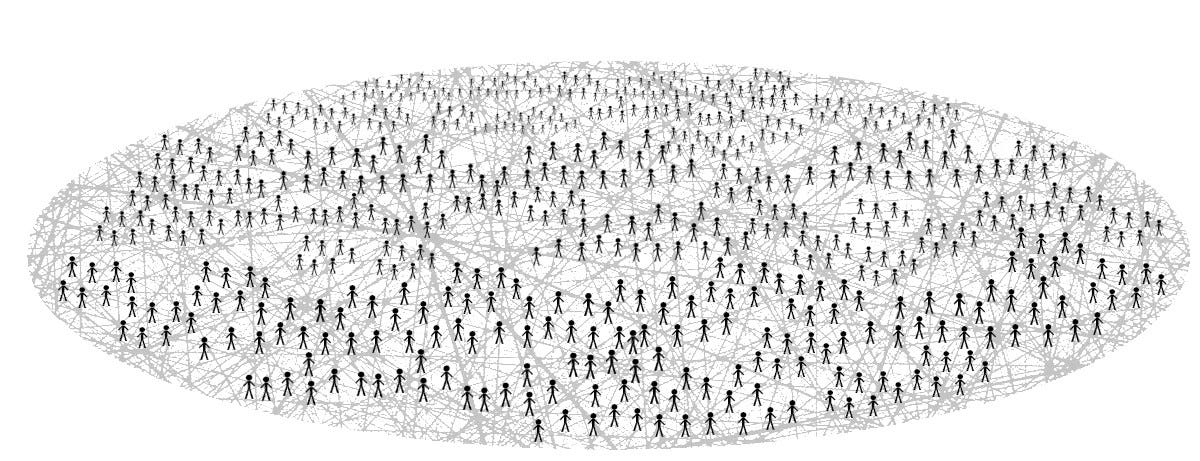

1: The interdependent economy

Let’s start with a meta point. All ‘economies’ throughout time are interdependent networks of people who draw upon the earth to survive. Interdependence, however, can be structured in different ways:

In the case of a hunter-gatherer band, we have a tiny, tightly knit network with relatively fixed and stable relationships. Life might be frugal, but you’re pretty much guaranteed a role in the society (i.e. you’re not going around begging powerful people for a ‘job’)

In the case of horticultural and pastoral tribal societies we have larger, more stratified groups, but the relationships remain relatively stable. You might enter positions through rites of passage, and be expected to take on certain roles

In the case of a feudal or caste-based society we have a much larger-scale, and also much more hierarchical system. It’s still interdependent, but there’s a distinct parasitism within it, with the top of the hierarchy skimming a lot from the bottom. That said, feudal systems have relatively fixed relations, which means there’s a degree of security for the people within it (think, for example, of the aristocratic statement ‘know your place’, which implies that there are set positions for different people)

In the case of modern capitalism we have a massive-scale, transnational network of people with insecure (fluid, breakable, reconfigurable) connections. People have to compete-to-cooperate (i.e. compete to forge connections, or compete to enter the society). Within this we find large inequalities in power developing, and the stratification of people into classes with highly unequal property ownership. In this sense it bears resemblance to feudalism, but is more fluid. You can be ejected from your position at any point (‘thrown out of the society’ as it were). This insecurity is cast as ‘freedom’ by ideological defenders of the system, and is imagined to be a source of dynamism (aka. if you have to constantly fight to stay in the society, you’ll constantly be on the lookout for ways to secure your place, and ways to secure advantage)

Let’s take that last system, and heavily abstract it by removing the inequalities in power, and just representing it as a big ‘horizontal’ network of interdependent people. The lines represent ties of interdependence, but these ties are being constantly reconfigured (e.g. if you decide to get bread from the local baker rather than the supermarket, you’re re-configuring a relationship of interdependence).

2: Money as a scaler

Traditional economics has a serious conceptual problem when it comes to money. 18th and 19th century economists basically looked at the image above - in which we have a large-scale network of strangers who are all entangled together - and then used it as an explanation for why money must exist.

I wrote about this in my piece How to Write a Flintstones History of Money, which explores presentism, the process in which you imagine the past as a half-formed version of the present.

In the case of traditional economists, this turns up in the notorious (and still very popular) ‘barter myth’, in which they imagine a scenario in which random strangers are trying to trade specialised goods in a market, but - somehow - have no monetary system, and so must clumsily ‘barter’ the goods, a situation that everyone finds very inconvenient, until they finally stumble on the ‘innovation’ of money to ‘solve’ the problem of barter.

In this worldview, economists basically imagine that large-scale, specialised markets full of strangers naturally exist, and then imagine money as a spontaneous invention that springs from the frustrated participants. This is a ‘solutionist’ account of money, in which it is imagined as a market solution to a pre-existing problem (for more on this, see Money as Addiction).

This is why anthropologists find mainstream economics ridiculous, because this isn’t a pre-existing problem. Tribal societies, for example, had many non-market ways of distributing goods, and were able to survive for a very, very long time without money, so all the imagined scenarios used to explain the ‘spontaneous’ market origin of money are largely ahistorical.

Here’s a metaphor to help you understand the conceptual error.

Imagine you see an elephant, and then you say ‘what would happen to this elephant if it had no nervous system?’ Then you say ‘well it would really struggle to coordinate its huge body’. Then you say, ‘oh, so the reason it has a nervous system is so that it can do that!’

What’s wrong with this? Well, the reason an elephant can have a large body with many moving parts is precisely because it already has a nervous system which has co-evolved with the body. You cannot use the presence of the body as an explainer for why the nervous system has come into being.

Similarly, you cannot use the presence of a large-scale market economy (full of strangers with specialist skills and diverse goods) as an explanation for why money exists, because - much like there is no world in which elephants walk clumsily around without nervous systems - there is no world is which we find large-scale networks of trading strangers without monetary systems already being present.

Unfortunately, that’s the exact fantasy used by traditional economists. They looked at the large-scale economies they were already in, and then said ‘what would happen if there was no money?’ This leads them to fantasise about an ahistorical scenario in which all the people have to now clumsily barter goods (the elephant without a nervous system), and then they use that to describe why money must have been ‘invented’ to make things easier. It’s like imagining a fully grown elephant ‘inventing’ a nervous system for itself to deal with the problem of being a fully grown elephant without a nervous system.

This fantasy in turn underpins broader commodity theories of money, in which the traditional economists speculate about which commodities would have the correct ‘natural’ features to deal with this ‘naturally occurring’ problem (for more on this, see The Archipelago). Not only are these commodity theories of money underpinned by an ahistorical thought experiment, but they often assume that humans are ‘naturally’ detached individual agents on markets, which is a modern ideology not a historical reality.

How do we disrupt this then?

Well, the first step is to invert the economist perspective, and say: money is not a ‘product’ of markets. Markets are a product of money.

I’m aware that this is a full pendulum swing to the extreme polar opposite view, and we don’t have to stay wedded to this, but - if you want to be able to think creatively about money - you have to open your mind to the possibility that it could pre-exist, or catalyse, or co-evolve with markets (much like the overall body of an elephant co-evolves with its nervous system). To do this, though, you basically have to be able to imagine that money might have a non-market origin.

I’m not going to pretend to give some robust historical account of this right now, but I’m going to ask you to entertain the idea that, rather than being something that spontaneously leaps out of markets of strangers, money is a political innovation that had the effect of creating markets of strangers, in particular by dissolving smaller interdependent groups who previously did not depend on money (e.g. tribal societies etc), and recombining them into larger, more diffuse interdependent networks that did.

In this framework, money is catalytic - it has a non-market origin, but sets in motion processes that start to snowball markets into being, which in turn feed back into greater need for money.

This process of dissolving smaller into larger is also associated with the rise of kingdoms and empires, so we should be prepared to look at money and state power as being ‘two sides of the same coin’, both acting in conjunction to break down older ways of being - such as tribal life - and to reconfiguring them into larger feudal, and then later market, societies.

Now, I’m well aware that this is glossing over a lot of stuff, but - remember - this is just a high-level alternative conceptual scaffolding for you to explore from (and it’s probably less bullshit that the high-level conceptual scaffolding traditionally used in standard economics).

3: MMT on the political foundation of money

So, having laid out that generic framework above, I’ll now note that MMT has a particular account of it. I’m not saying that all MMT economists agree on all the exact details, but the basic idea is that:

Money is a political innovation, rather than the spontaneous market invention

That it has a role in catalysing large-scale markets that otherwise wouldn’t naturally exist

And, as a result of this, there is no hard distinction between State and Market (which is a core dogma within much traditional economics and libertarianism etc)

From here, there is a more specific MMT-ish claim, which is that money is something used by warlords as an alternative means of extracting resources from a population, rather than merely pillaging them.

It’s worth noting that this style of thinking is not unique to MMT. Anthropologists like David Graeber have made similar claims (for example, in his book Debt: The First 5000 Years).

Rather than the direct, explicit violence of riding in and looting stuff, there’s a switch to indirect, implicit violence in the form of a pseudo-‘exchange’, in which the warlord sovereign issues credits to subjugated people in exchange for real goods and services.

The way that the sovereign gets the people to take the credit in the short-term, though, is to demand it back from them in the long term (with the threat that if they fail to hand it back, violence awaits)

In the MMT framework, taxation is seen to have this function. A government doesn’t tax to ‘raise’ money’, but rather to artificially create demand for the money that it will issue out to get things

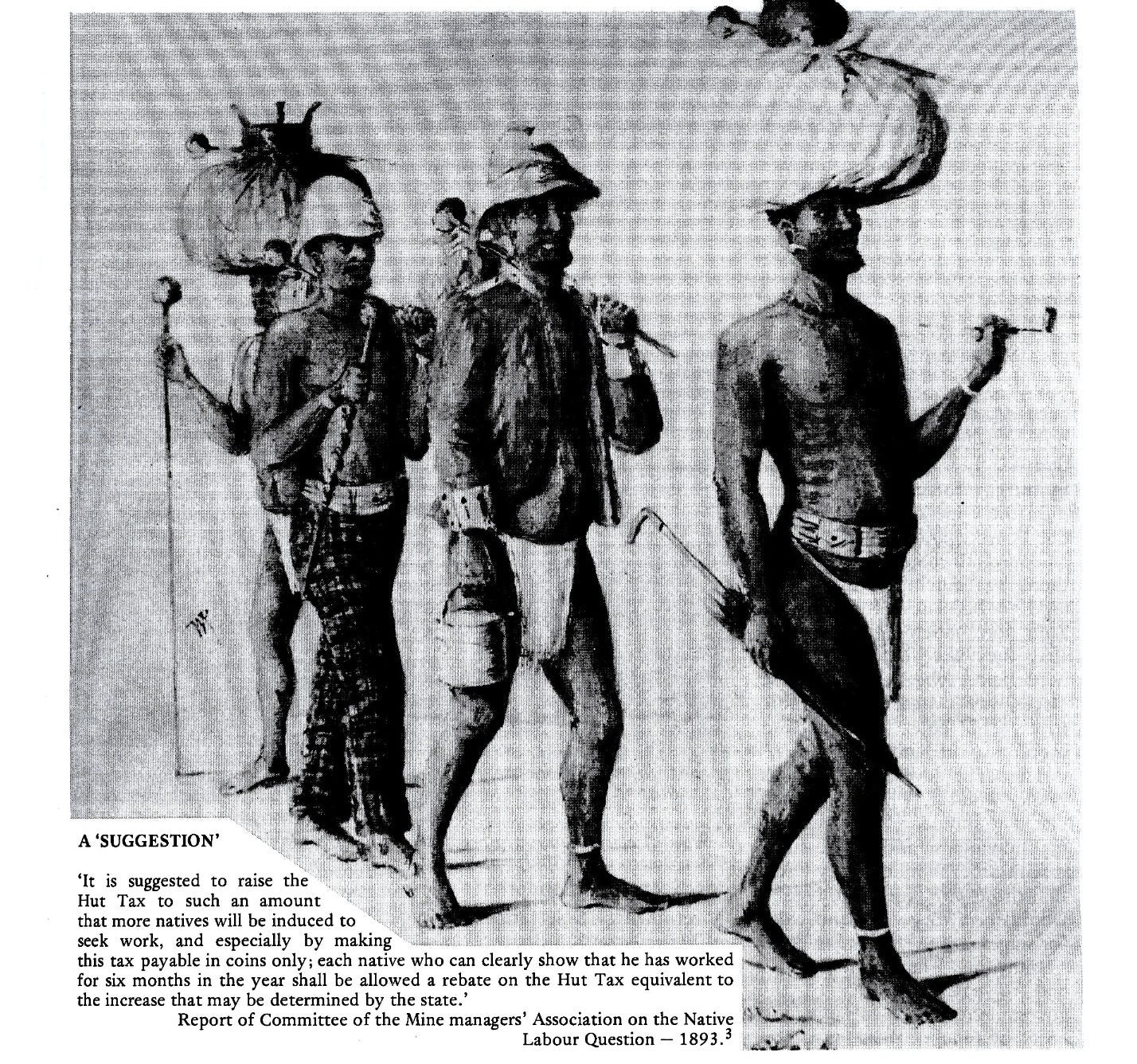

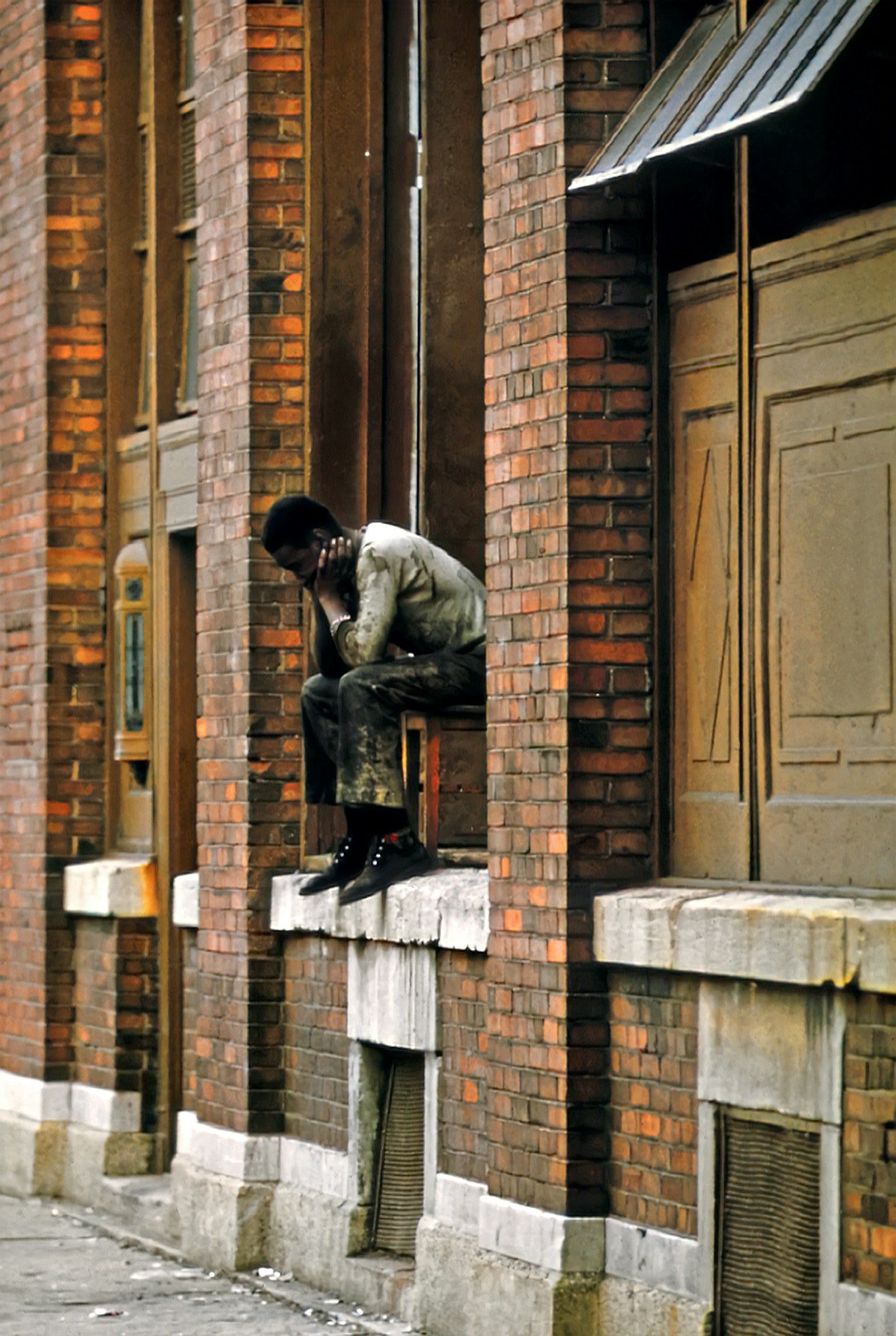

Here’s a concrete example from my birth country South Africa, to help make this clearer. Let’s talk about colonial ‘Hut taxes’.

In 19th century South Africa we find tribal Zulu people living in non-monetary economies. Colonial authorities, however, wanted them to work in the mines, but tribal people did not depend upon money, and so had little requirement, or desire, to go ‘get a job’ in the mines.

It would of course be possible for the colonial sovereign to simply force them to work in the mines, but that’s a risky gambit that can easily lead to uprisings. The more indirect and subtle method was to impose a ‘Hut Tax’, telling the Zulu people that they had a tax obligation, which requires them to hand in money credits at some point in future, and that they would be punished if they didn’t.

This creates artificial demand for the credits. The Zulu people must now go find the credits, but where? Well, the bosses of the mines have them, so the Zulu people must now labour to get them from the bosses. The net effect is that the colonial sovereign gets labour, and the Zulu get credits, which they later must hand back to settle the Hut Tax.

Just in case you don’t believe this, read the inscription on the image above, where the mine managers literally spell it out.

“It is suggested to raise the Hut Tax to such an amount that more natives will be induced to seek work, and especially by making this tax payable in coins only”.

This is a fairly recent example, but this basic principle extends back in time. Taxation by ruling monarchs has this effect of pulling subjugated people into dependence on money.

The two lives of money

So, in this framework, money has a primary life and a secondary life

In its primary form, money credits are a political tool used by a sovereign to extract stuff from a population. This is the true meaning of ‘seniorage’: it’s the actual labour and resources obtained by a state in exchange for issuing credits

This, however, gives rise to a secondary life for money, in which it starts to get used between ordinary people. This can come from at least two sources

The taxation obligation (e.g. the Hut Tax) is imposed across the board, which means that if you don’t wish to work for the sovereign, you must find the credits from someone else who will. Picture a Zulu pastoralist trying to enter into a tit-for-tat deal with someone who has been working in the mines, in order to obtain the credits

Because a common system of credits is now moving across territories that might have previously hosted relatively discrete smaller-scale economies, we find that relative strangers are now able to engage in low-trust interactions with each other. The common credits issued out by the almighty, distant, sovereign, can breach previous boundaries between different groups, allowing for arms-length forms of market exchange to spread

The basic picture then, is one in which these political credits start to catalyse larger scale market structures. Over time, the primary political origins of these credits get obscured as that secondary market life takes root. They begin to appear as ‘economic’ ‘means of exchange’.

This benefits sovereign powers, because as large-scale markets start to boost up production, the sovereign ends up with more stuff being produced than if they were merely pillaging existing stuff (a process that undermines production and which isn’t a lasting, sustainable source of extraction).

So, fast-forward into the modern era, and the moral of the story is that state power, money, markets and capitalism are all intertwined.

With this in mind, we can start to see that the imagined battles between The State vs. The Market (e.g. as imagined by Reagan and Thatcher) are just shallow modern skirmishes between two inextricably linked factions of the same system. ‘Free markets’ are an ideological fantasy hallucinated by capitalist elites whose billions would not exist without state structures, but who constantly want the state to back off (a bit like a young teenager who fantasises about running away from home to escape their parents).

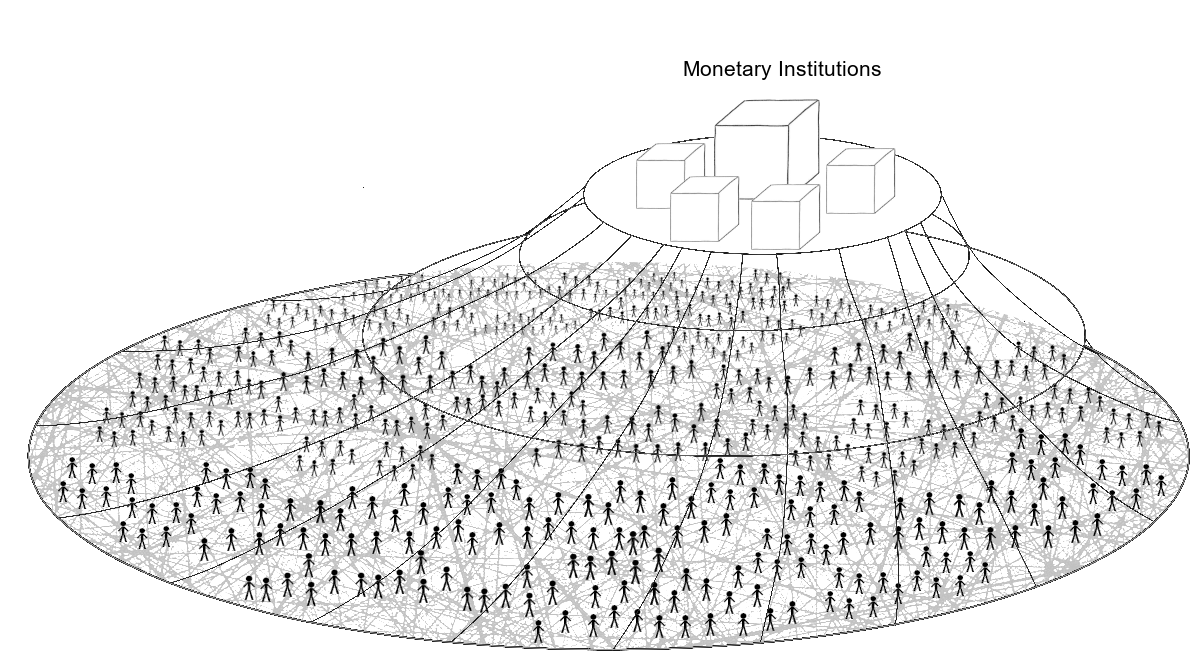

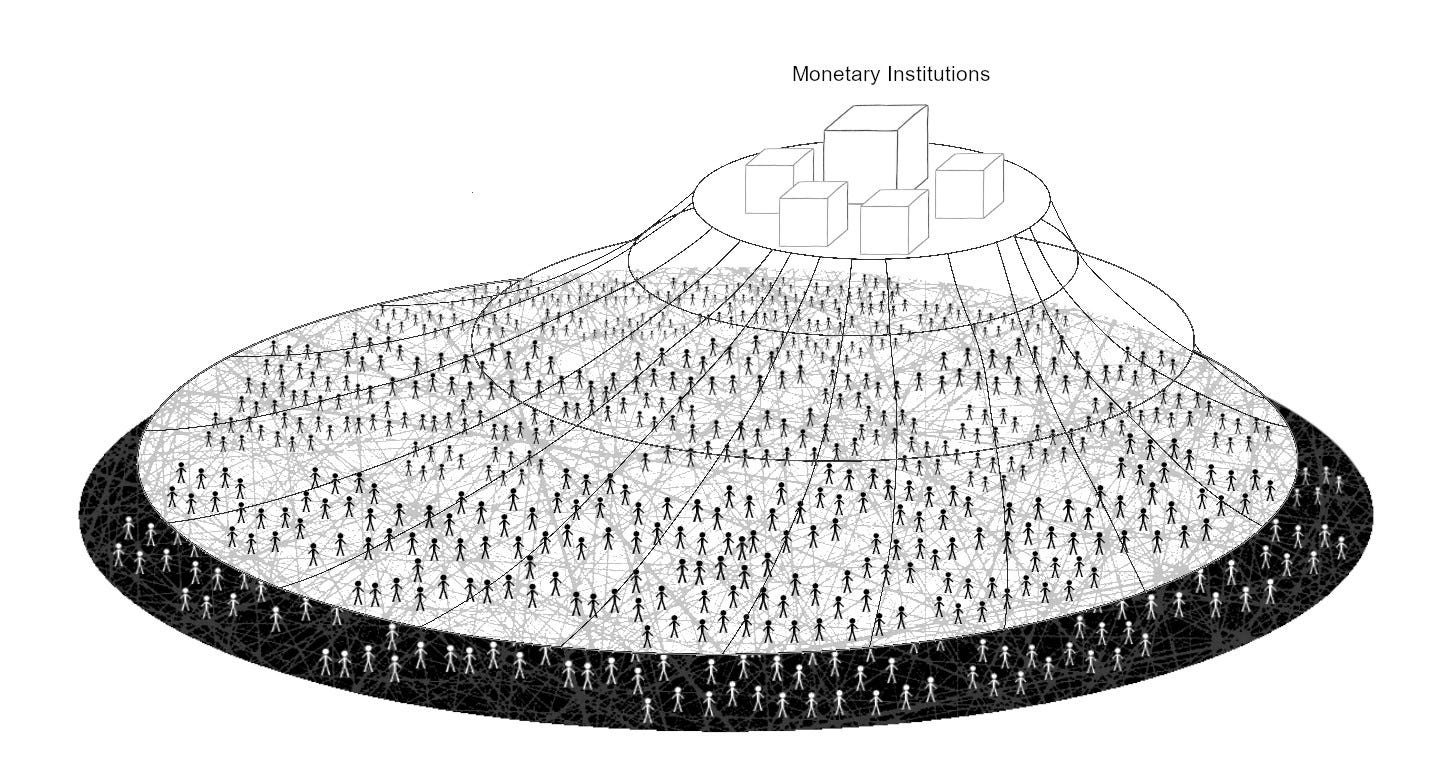

So, let’s bring this full circle, and superimpose the aforementioned ‘double-life’ of money over our ‘horizontal’ interdependent network we started with. We now have two dimensions:

Money issuers occupy a vertical dimension, issuing money down to ordinary money users, and pulling it back up (DISCLAIMER: this is a piece about state money issuance, and I’m going to avoid talking about bank money issuance here - for anyone who wants to pick that thread up, see this piece)

Money users occupy the horizontal dimension, using the vertically issued credits horizontally between themselves as a means to forge and maintain ties of interdependence

4: Proletarianization

Having described some politico-economic mechanisms via which monetary markets can start to take root, we can then start to talk about network effects in which the markets grow and begin to take over, and eventually hit a tipping point in which they suck people in, and eventually become mandatory.

In Marxist speak, this gets described as proletarianisation: the process by which people who previously did not depend on fluid capitalist markets are (often forcibly) integrated into them. After this happens, survival becomes tied to doing deals with total strangers via money systems.

This often goes hand-in-hand with the removal of alternative ways of being, such as the removal of common land. This is why Marxists spend a lot of time talking about the Enclosures - a historical period in which European elites wrested control of common land and privatized it, thereby creating ever more pressure for peasants to leave the land and drift into subordinated positions within urban markets as a landless ‘working class’. Picture those 18th and 19th century images of people crowding into city slums, and facing destitution if they failed to secure a role in the Dickensian factory owned by some powerful magnate.

Let’s focus on two elements of the picture here:

Entering the market network is becoming mandatory as people lose alternative means of survival. In libertarian fantasies of ‘free markets’ there’s an implicit assumption that there is an exit option, as if a person simply had the capacity to live a self-sufficient life outside the market, and that the market is therefore voluntary. This is totally bogus, because the vast majority of people cannot just detach themselves from society and live in the wilderness by themselves, so must find a way to fuse into the market system

A huge amount of insecurity emerges from this, as people must cling for any connection into the market they can find. If they can’t, they end up crowding around on the outskirts of it, trying to get in (a bit like a kid who want to get picked for the team but who find themselves increasingly desperate as all the positions get filled up)

From a political perspective, this creates the conditions for class conflict. Those most able to offer access to the network are those who own ‘capital’, or productive assets (the proverbial factory), but this puts them into a position to exploit those who have a mandatory requirement to enter. ‘Capitalists’ like this can get the precarious working class to hand over much of what they produce as a type of rent for the privilege of entering the market, a process that yields even more to those with capital, who can in turn reinvest that to further dominate the productive assets (a process that culminates in what Marxists would call ‘owning the means of production’).

This is why we have a fundamental ideological disagreement between those with a libertarian view and those with a Marxist view. The libertarian view imagines that market interactions are all voluntary and ‘free’, whereas the Marxist view would argue that this freedom is illusory, and that it disguises a deeper process of systematic rent extraction in which wealth flows from those who work to those who own (hence, the concept of Labour vs Capital).

5: Money as a means of connection

We are trained to imagine that market systems are primarily systems of competition, but it’s crucial to primarily imagine them as systems in which people compete-to-collaborate. This ‘cooperation’ is not necessarily egalitarian - for example, when workers are competing for a job, they are often fighting for the right to cooperate with a capital owner, but this can simultaneously be the act of fighting for the right to be exploited.

Nevertheless, regardless of whether it is parasitic or mutualistic, interdependence is the prime reality of all economic systems, but in large-scale market systems this is obscured simply because of the sheer insecurity (and scale and modularity) of the interdependent structure. This means perceptions of ‘independence’ rise: a person perceives themselves as a solo individual, fighting to get in.

So, at an ontological level, a capitalist market system is de facto interdependent (albeit with many parasitic elements), but - at a phenomenological level - it often doesn’t feel like that. You feel detached, as if you were a solo atom, because - firstly - you literally do have the option to constantly detach from one producer and re-attach to another, but - secondly - that same thing can be applied to you as a producer by others. There is no fundamental security of place. Not only do you have to fight to get into the structure, but you have to fight to stay in.

At this point it’s worth reiterating that conservative economists wish to characterise this non-voluntary and often precarious structure as simply being the spontaneous outcome of daily voluntary decisions by independent self-contained individuals who ‘choose’ to come together to trade to pursue their mutual self-interest (think, for example, of Thatcher’s infamous saying ‘there is no such thing as society, there are only individual men and women). This background imagination, in turn, leads us back to commodity theories of money: conservatives have an in-built ideological tendency towards wanting to see money as some kind of apolitical commodity that these imagined individuals use to induce each other to trade.

This is also why standard economists try to use these models in which money is described as some kind of rational tool with obvious ‘functions’, and one of those imagined functions is that it is a ‘means of exchange’.

Once we move past the background conservative imagination that informs that description, however, and move towards seeing markets as politically-underpinned, non-voluntary, fluid structures of interdependence that are preceded by money, those economistic ‘functional' descriptions of money start to break down.

In fact, the only functional description I’d ever use for money is to say it’s a ‘means of connection’ to an interdependent network. If I was putting it into quasi-metaphorical terms, I’d say that money is the means via which you ‘dock’ into the structure. In other words, you are fusing with someone when you’re handing over money to them, but disconnecting from them when you don’t. So, when I buy bread from the supermarket rather than the local baker, I’m cutting off my collaboration with the latter and re-forging it with the former.

Needless to say, once proletarianisation has occurred, we have loads of people clamouring to enter the network, a process in which they wish for people to fuse with them by offering credits in exchange for labour, and then using the resultant credits to fuse into others to get things they need.

6: The concept of “unemployment”

In a hunter-gather band, ‘unemployment’ is not really a thing. You don’t find the members of the historical Hadza or ǃKung people trying to convince each other to give each other ‘jobs’ in order to get credits to redeem back for part of the communal hunt. Rather, there are relatively safe roles, clear paths to get into them, and non-monetary means of distributing things collectively produced.

Unemployment, though, is a very real phenomenon in monetary market systems. It basically refers to those situations in which a person depends on the network but cannot fuse into it, primarily because nobody is willing to become dependent on them (to ‘fuse’ into them, as it were)

In the case of adults, these are people who want and need to enter but who can’t, and are therefore cut off from their means of survival

Kids, who nowadays aren’t allowed to enter, get called ‘dependents’ rather than ‘unemployed’. They have to be tethered to another person who has a place in the network. At some point, the kids will come of age and will join the ranks of the unemployed looking for entry

Let’s represent the unemployed as a shadow ring of people around the network, trying to get in, with hypothetical but dormant ties of interdependence that have not been activated as it were.

This helps us to see some of the power dynamics of historical capitalism: an urban working class has nowhere else to go for safety, so not only can they be exploited by those with capital, but they also pose a problem for authorities if they remain ‘idle’, because they may become desperate, and might be pushed toward crime (for example, forcibly extracting goods from the elites of the network), or ‘black market’ activity.

Hard conservatives have a tendency to imagine that the poor and unemployed are just dangerous deviants that have only themselves to blame, and that they need to be controlled by firm Law and Order (think about the rhetoric that surrounds ICE agents in the US). That said, the rise of capitalism has also historically been accompanied by the rise of liberal reformers who were often concerned about the plight of the urban poor, and this continues to this day (for more on liberal reformism, see Making Capitalism Bad Again).

Having noted that this shadow zone of unemployed people poses serious problems, it also represents an opportunity for the overall system to expand, as capitalists - and others - can draw upon this unused labour pool for new production.